Netflix still rules, but Singapore’s streaming scene is getting crowded

New Q1 2025 data from JustWatch reveals growing competition in Singapore’s streaming market

Singapore’s streaming market is showing signs of a power shift.

While Netflix held onto its lead in Q1 2025, new data from streaming guide JustWatch shows that challengers like Disney+, Prime Video, Max, and Apple TV+ are quietly closing the gap.

This article explores the Q1 2025 SVOD (subscription video-on-demand) market share data for Singapore, drawing on the viewing behavior of 60 million monthly JustWatch users globally—including local trends from over 140 countries.

For brands and marketers in APAC, this update signals changing audience behaviors that could impact content partnerships, advertising budgets, and OTT strategies.

Short on time?

Here’s a table of contents for quick access:

What the Q1 2025 data shows

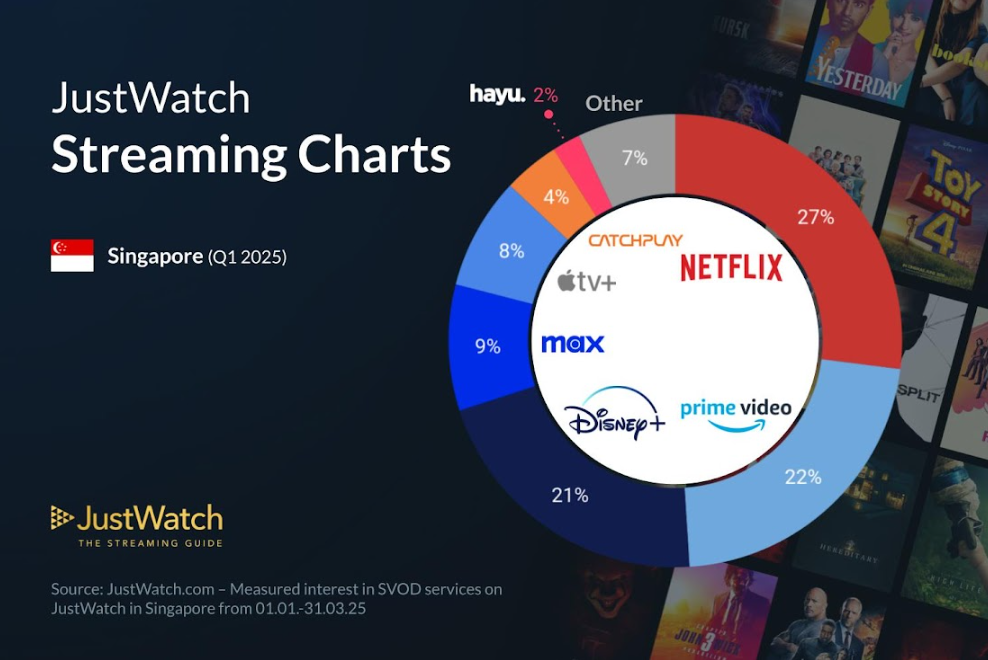

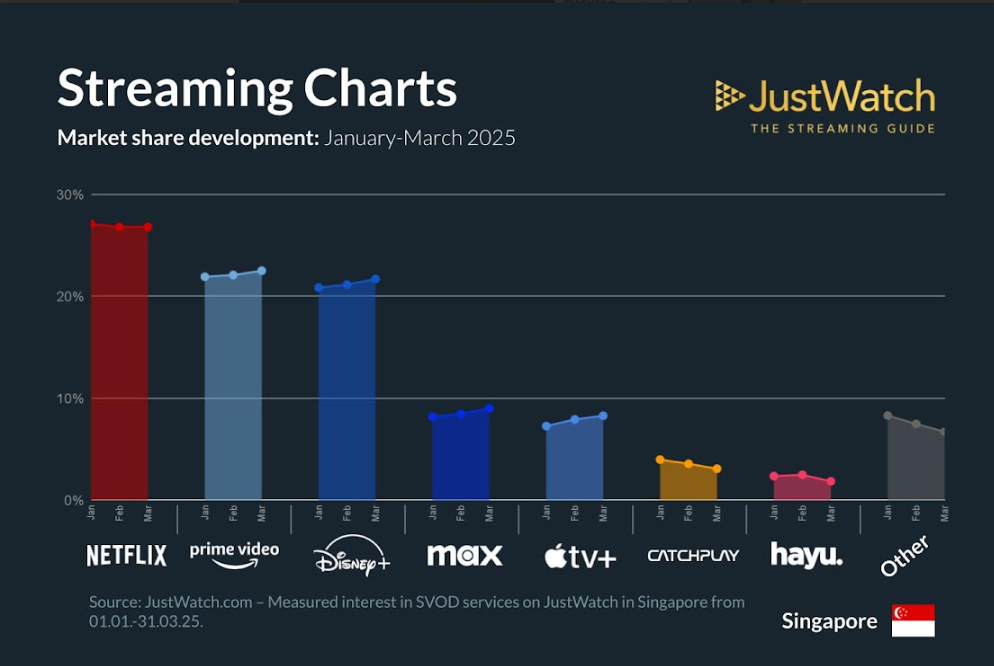

In Singapore, Netflix maintained the largest SVOD market share in Q1 2025, but the real story lies in the movement below the top line.

JustWatch’s report shows that Disney+, Prime Video, Max, and Apple TV+ each gained a +1% share compared to previous quarters. That’s modest growth on paper—but in a market as competitive as Singapore, even single-digit gains can signal shifting loyalties or new user acquisition wins.

These four players are riding positive momentum, possibly fueled by broader global pushes in content catalog expansion, regional partnerships, or pricing strategy updates that appeal to Singapore’s digitally native, subscription-savvy consumers.

Who's losing ground in Singapore?

Meanwhile, smaller platforms like Hayu and Catchplay are losing traction, with both dropping -1% in market share in Q1.

This mirrors a broader trend: niche or single-genre services struggle to hold user attention when larger platforms diversify their libraries and invest in original local content.

Netflix, interestingly, didn’t gain or lose ground—suggesting a saturation point or stable retention in the market.

For marketers, this "steady at the top" status means Netflix may no longer be the growth story, but rather a baseline to benchmark other platforms against.

What marketers should know

1. Platform diversification matters

Singaporean audiences are exploring beyond Netflix. This suggests opportunities for brands to diversify OTT media buys, especially with platforms like Disney+ and Prime Video showing growth.

2. Netflix’s dominance comes with new creative opportunities

While Netflix remains the top streaming platform, the bigger opportunity may lie in its new AI-powered ad formats that let brands integrate directly into hit shows like Stranger Things and Emily in Paris. This modular framework gives marketers a faster, more scalable way to align with premium IP—without traditional production costs or long lead times. For APAC marketers, this could be a smart way to tap into cultural relevance while staying efficient.

3. Local partnerships could yield high ROI

Global platforms are increasingly seeking regional relevance. For content marketers or PR pros, this is a prime time to pitch local productions, influencer tie-ins, or product placements in growing platforms like Max and Apple TV+.

4. Smaller platforms face consolidation pressure

Hayu and Catchplay’s dip points to potential consolidation or niche repositioning. Marketers should watch for shifts here—either in M&A activity or strategic pivots that may open up B2B content collaborations.

5. SVOD is part of a larger attention economy

The steady gains of second-tier players may also reflect shifting screen time from social platforms or linear TV. A cross-channel strategy that includes streaming, short-form video, and owned content hubs may be necessary to capture attention throughout the funnel.

Q1 2025’s streaming data tells a familiar story with a new twist.

Netflix may still sit on the throne, but challengers are building their case—and audiences are responding. For marketers, this is the moment to rethink which platforms deserve your attention, ad dollars, and strategic partnerships.

With mid-2025 on the horizon, the platforms that continue gaining share could soon redefine what "premium content" and "streaming engagement" mean in APAC.