TikTok Shop strategy for brands in Southeast Asia: what works in 2026

What brands entering TikTok Shop SEA need to know in 2026

TikTok Shop is no longer an emerging channel in Southeast Asia. It is the region's fastest-scaling commerce platform, and brands that are still "evaluating" it are ceding ground to competitors who moved earlier.

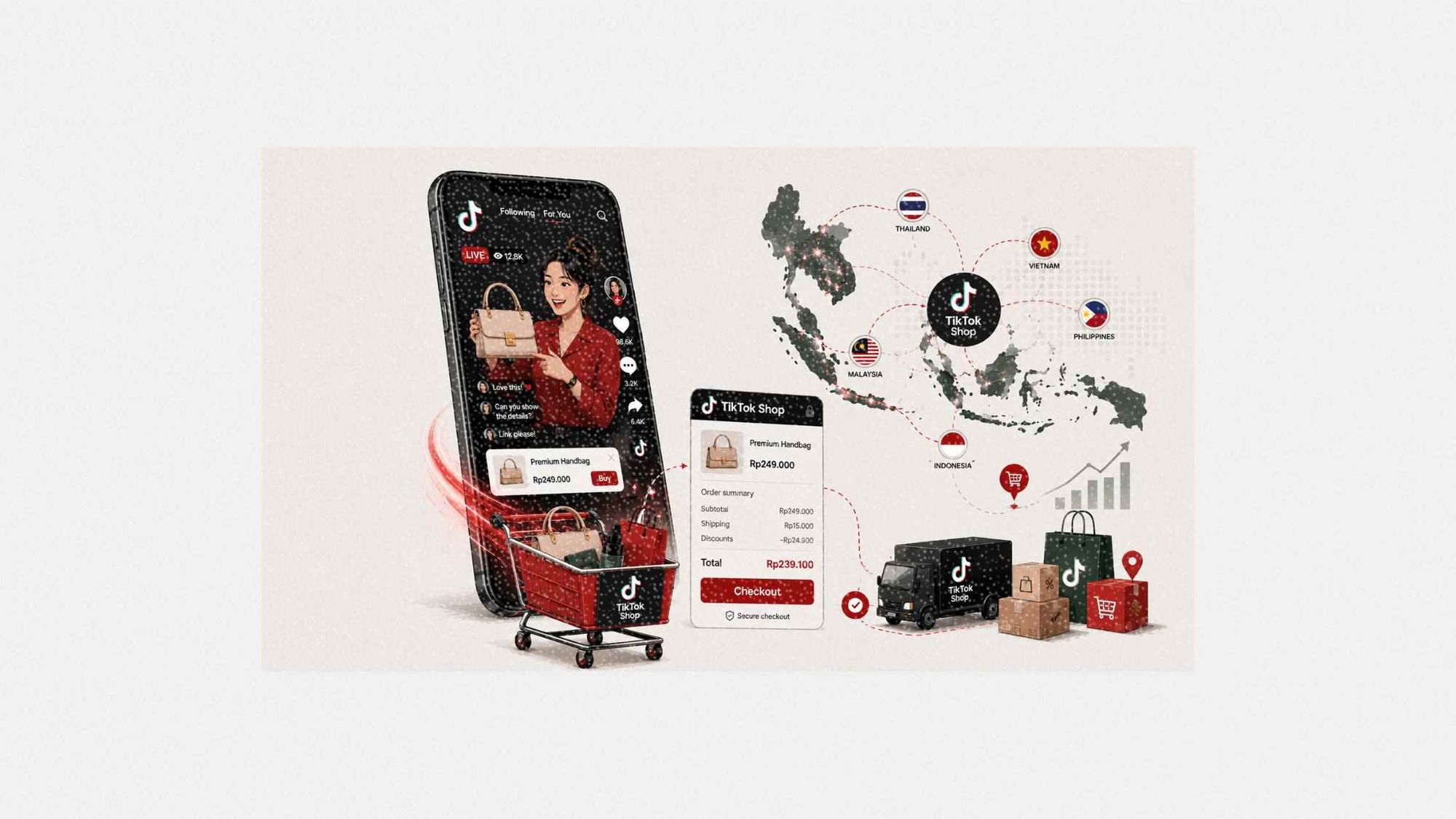

According to Momentum Works, TikTok Shop's Southeast Asia GMV doubled year-on-year to US$45.6 billion in 2025, representing 71% of the platform's total global GMV of US$64.3 billion. Every major SEA market posted triple-digit growth. Indonesia alone reached US$13.1 billion, making it TikTok Shop's second-largest market globally.

The brands winning in this environment are not running the same influencer playbook they use elsewhere. They are adapting to a distinct creator ecosystem, a live-commerce-first format culture, and market-by-market dynamics that behave very differently from each other.

This guide covers what that adaptation actually looks like.

Table of contents

Jump to each section:

- Why TikTok Shop is SEA's fastest-growing commerce channel

- From KOL to KOS: the creator shift redefining SEA campaigns

- Market by market: TikTok Shop dynamics across Southeast Asia

- Live commerce: the format driving the most GMV in the region

- How to build a TikTok Shop creator program for SEA

- Common mistakes brands make when entering TikTok Shop in Southeast Asia

Why TikTok Shop is SEA's fastest-growing commerce channel

The headline growth numbers are striking, but the structural story underneath them matters more for brands planning market entry or expansion.

TikTok Shop grew from US$4.4 billion in SEA GMV in 2022 to US$45.6 billion in 2025, a ten-fold increase in three years. That velocity did not come from a single market. According to data compiled by Digital in Asia, every major SEA market doubled year-on-year in 2025: Indonesia grew 111%, Thailand 101%, Vietnam 150%, Malaysia 132%, and the Philippines 99%.

This is not a platform gaining incremental share. It is creating net-new commerce behavior, reaching buyers who had not previously transacted online through traditional e-commerce platforms. That is the opportunity most brands are underestimating.

The mechanism behind it is discovery-led commerce. Unlike Shopee or Lazada, where buyers arrive with purchase intent, TikTok Shop converts passive scrollers into buyers within a single session. A product video that hooks a viewer in three seconds can close a sale in under two minutes through an in-app checkout. The commercial logic is completely different from search-based or catalogue-based e-commerce, and the creator strategy needs to match it.

At the Q4 2025 peak shopping period, according to Cube's Tradewinds data, TikTok Shop achieved 82% year-on-year GMV growth, its strongest quarter on record, precisely when the highest commercial stakes are on the table.

From KOL to KOS: the creator shift redefining SEA campaigns

The biggest conceptual shift for brands entering TikTok Shop SEA is understanding that the creator types driving GMV are not the same creators who drive brand awareness on Instagram.

Traditional influencer marketing relies on Key Opinion Leaders (KOLs): creators with audiences who trust their taste, personality, and recommendations. KOL campaigns work for brand equity, consideration, and longer purchase cycles.

TikTok Shop's top GMV drivers in Southeast Asia are increasingly Key Opinion Sellers (KOS): commerce-first creators whose entire output is oriented toward immediate conversion. They anchor products on camera, demonstrate use in real time, handle objections live, and guide viewers to checkout within minutes.

As documented in Cube's Influencer Marketing in Southeast Asia 2025 report, KOS growth is accelerating rapidly across the region, especially on TikTok Shop, and over 80% of SEA consumers have made purchases through affiliate-linked creator content.

This does not mean KOLs have no role on TikTok Shop. They remain valuable for product launches, brand storytelling, and seeding content that feeds the platform's discovery algorithm. But brands that run a pure KOL strategy on TikTok Shop and expect it to generate meaningful GMV will be disappointed. The creator mix needs to reflect the platform's commerce mechanics, not the brand's existing influencer roster from other channels.

Dinda Anandita, Account Director at content-led comms agency Content Collision, puts it directly: "The mistake we see constantly is brands briefing TikTok Shop creators the same way they'd brief an Instagram influencer. They're asking for beautifully shot content with brand messaging, but the creator's audience came to that livestream to buy something, not to watch an ad. The brief needs to start with the sales moment, not the brand story."

Market by market: TikTok Shop dynamics across Southeast Asia

One of the most important things to understand about TikTok Shop SEA is that it is not one market. The platform's behavior, dominant categories, and creator norms differ meaningfully across each country.

According to AnyMind Group's State of Influence in APAC 2026 report, drawing on nearly 7,000 campaigns across the region, TikTok is the dominant influencer platform in Thailand (66% of campaigns), the Philippines (64.3%), and Vietnam (62.9%). In Malaysia, the split is more even, with Instagram at 47.7% and TikTok at 44.4%. Across Southeast Asia as a whole, TikTok's share of influencer campaigns grew from 28.35% in 2023 to 50.58% in 2025.

At the market level, the platform dynamics break down roughly as follows.

Indonesia is TikTok Shop's largest SEA market and its second-largest globally, generating US$13.1 billion in GMV in 2025. The TikTok Shop-Tokopedia integration (following ByteDance's 2023 acquisition of a controlling stake in Tokopedia) gives the platform unique credibility among Indonesian sellers and buyers who trust Tokopedia's established logistics rails. Beauty, fashion, and health products dominate. Campaign content tends to perform better when it feels raw and authentic rather than polished.

Thailand reached an estimated US$10 to 12 billion in GMV in 2025, with Q1 growth tripling year-on-year per Momentum Works data. Live commerce is deeply embedded in Thai consumer behavior. The top-performing creators are overwhelmingly sales-oriented, and the fastest-growing TikTok Shop categories include beauty, supplements, and household goods. Brands that enter Thailand with a "brand awareness first" mindset often underperform against local sellers who treat every session as a selling event.

Vietnam is the fastest-growing major SEA market on TikTok Shop, posting roughly 150% GMV growth in 2025. The audience skews young, mobile-first, and highly responsive to price signals and live promotions. Authenticity and local language fluency from creators matter more here than production quality.

Malaysia operates with the most balanced platform mix of any major SEA market. Because Instagram remains competitive, brands should not treat it as a pure TikTok-first market.

The Philippines has the highest social media engagement rates in the region and is among TikTok Shop's fastest-growing markets in terms of creator participation, though average order values are lower than in Thailand or Indonesia.

Singapore's TikTok Shop presence is smaller in GMV terms but functions as a premium brand entry point. Consumers here are more research-led, and influencer content tends to pair better with a strong brand narrative.

Live commerce: the format driving the most GMV in the region

If you want to understand where TikTok Shop GMV is actually generated in Southeast Asia, the answer is live commerce.

Unlike the United States, where video content currently accounts for around 50% of TikTok Shop GMV and live commerce is at 14%, Southeast Asian markets show a much more balanced split across video, live, and Shop tab formats, with live commerce holding a consistently significant share. Markets like Thailand and Vietnam are live-commerce-first environments, where multi-hour selling sessions are the norm rather than the exception.

For brands, this means several things.

Creator selection changes. A creator who produces excellent short-form video content may have limited live-selling ability. Live commerce requires a different skill set: the ability to speak for extended periods, manage product demos in real time, respond to audience questions, and create urgency without scripting. These are sales skills as much as content skills.

Scheduling matters. Live sessions in peak evening windows (typically 8 to 10 pm local time) generate disproportionate GMV in most SEA markets. The best-performing sessions are planned around promotional hooks, voucher drops, and limited-time offers, not just product demonstrations.

Production quality is lower than many brand teams expect. Polished, studio-produced live sessions often underperform raw, kitchen-table authenticity in SEA markets. The format rewards perceived realness, and audiences are sophisticated enough to feel the difference between a genuine seller and a brand-managed broadcast.

For brands that also manage their own creator programs elsewhere, the live commerce requirement means rethinking what "ready to activate" means. A creator with 200,000 TikTok followers who has never run a live selling session needs onboarding and coaching before they generate ROI on TikTok Shop.

How to build a TikTok Shop creator program for SEA

A functional TikTok Shop creator program in Southeast Asia requires different inputs than a standard influencer campaign. Below is how the structural elements differ.

Creator sourcing should start inside TikTok Shop's own affiliate marketplace, not from external influencer databases. TikTok Shop's built-in affiliate program connects brands with creators who have already demonstrated commerce intent on the platform. These creators often have smaller followings than traditional KOLs, but their conversion track record on the platform is directly observable.

Commission structure matters more than flat fees. The most effective TikTok Shop creator programs in SEA use a hybrid model: a modest flat fee to secure content commitment (and cover a creator's time for live sessions), plus a commission per sale. Commission rates by category typically range from 4% to 13%, with beauty and supplements at the higher end and electronics at the lower end. This aligns creator incentives directly with brand outcomes.

Tier diversification reduces risk. Depending on a single macro creator to drive TikTok Shop GMV is a structural mistake. The most resilient programs spread activation across 10 to 30 micro and nano creators, which also gives the algorithm more content surface area to test and distribute.

Market-specific creative briefs are non-negotiable. A brief built for an Indonesian campaign (favor authenticity and affordability signals) will not perform in Singapore (where brand quality and trust signals matter more). Localization goes beyond language to include the visual aesthetic, the pace of content, and the pricing psychology that resonates with each audience.

Track through TikTok Shop's native attribution, not just external UTMs. The platform's affiliate dashboard provides closed-loop attribution from content view to purchase, which makes ROI reporting cleaner than almost any other social commerce channel. Brands that do not enable this are flying blind.

Common mistakes brands make when entering TikTok Shop in Southeast Asia

For context on how not to approach TikTok Shop SEA, these are the patterns that consistently underperform.

Treating it as a paid media channel. TikTok Shop Spark Ads and affiliate programs require creator content to work. Brands that try to push product catalogue ads without creator relationships rarely achieve the discovery-loop GMV that the platform enables.

Applying a single regional strategy. A unified SEA playbook, with the same creator mix, pricing, and content style across Indonesia, Thailand, Vietnam, Malaysia, and the Philippines, will underperform in all five markets. Country-level planning produces meaningfully better outcomes.

Prioritizing follower count over commerce track record. On TikTok Shop, a creator with 50,000 followers and six months of live-selling experience will typically outperform a creator with 500,000 followers who has never run a live session. Platform metrics matter more than vanity metrics.

Skipping localization. Content filmed in a language or cultural register that does not match the target market will be deprioritized by the algorithm and ignored by audiences. This applies not just to language but to product framing, pricing references, and the cultural norms of how trust is built in each market.

Managing TikTok Shop from a global hub without local execution capability. The markets with the strongest TikTok Shop results have in-market teams or local agency partners who can run live sessions, manage creator relationships, and respond to platform changes in real time.

TikTok Shop in Southeast Asia rewards brands that treat it as a commerce infrastructure investment, not a campaign. The brands getting the most out of it have a creator roster they build over time, a live commerce capability they develop iteratively, and a market-by-market approach that matches platform behavior in each country.